Bitcoin: The Digital Currency Revolution

An exploration of Bitcoin, covering its origin, blockchain technology, mining process, and role in the financial ecosystem. This chapter delves into Bitcoin wallets, transactions, security practices, exchanges, and its regulatory landscape, while also addressing scalability issues and potential solutions like the Lightning Network.

- Bitcoin Blockchain Wars and Its Evolution: Implications for Decentralisation, Economics, and Governance

- The Bitcoin Reformation

- Bitcoin Knots

- 📊 Bitcoin Price Projections Based on Asset Class Market Caps

- 📜 BIP-119 (CTV): A Potential Upgrade to Bitcoin

- Separation of Money and State

- The Weaker the Dollar, the Louder Bitcoin Roars

- 🧭 The Full Bitcoin Club

Bitcoin Blockchain Wars and Its Evolution: Implications for Decentralisation, Economics, and Governance

The Bitcoin Blockchain War (2017): A Turning Point

The Conflict:

As Bitcoin’s popularity surged, its scalability was questioned. The network’s 1 MB block size limit, introduced in 2010, restricted transaction throughput to 3–7 transactions per second, leading to delays and high fees during peak demand.

Two factions emerged:

-

Block Size Increase Advocates:

-

Believed Bitcoin should scale on-chain by increasing the block size, enabling more transactions per block.

-

Argued that larger blocks would reduce transaction fees and support Bitcoin’s use as a peer-to-peer electronic cash system, consistent with Satoshi Nakamoto’s original vision.

-

Viewed concerns about centralization as overstated, asserting that technological advancements in storage and bandwidth would mitigate increased node costs.

-

Criticized second-layer solutions like the Lightning Network as overly complex and potentially centralizing due to the reliance on custodial hubs.

-

-

SegWit and Lightning Supporters:

-

Proposed keeping the block size small to preserve Bitcoin’s decentralization.

-

Emphasized that larger blocks would increase the cost of running a full node, reducing the number of participants and risking centralization.

-

Advocated for Segregated Witness (SegWit) to optimize block usage and enable second-layer solutions like the Lightning Network for off-chain scaling.

-

Argued that a decentralized network was essential to Bitcoin’s resistance to censorship and long-term viability.

-

The Split:

The disagreement culminated in a hard fork in August 2017, resulting in two chains:

-

Bitcoin (BTC):

-

Retained the 1 MB block size, adopted SegWit, and shifted toward a "store of value" narrative akin to digital gold.

-

-

Bitcoin Cash (BCH):

-

Increased the block size to 8 MB (and later 32 MB), focusing on low-cost, high-speed transactions to maintain Bitcoin’s usability for payments.

-

Implications:

-

By limiting block size, BTC ensured decentralization by keeping the requirements for running a full node accessible. However, this choice constrained Bitcoin’s capacity as a global currency.

-

BCH sought to enhance usability for everyday payments but sacrificed some decentralization, as larger blocks demand more resources, potentially centralizing the network over time.

-

BTC’s approach also facilitated second-layer scalability solutions like the Lightning Network, designed to handle microtransactions off-chain while maintaining the integrity of the base layer.

The Bitcoin Cash Fork (2018): Further Fragmentation

Dispute Over Direction:

Bitcoin Cash itself split into Bitcoin Cash (BCH) and Bitcoin SV (BSV) in November 2018.

-

Bitcoin SV (Satoshi’s Vision):

-

Championed by Craig Wright and Calvin Ayre, this chain implemented massive block size increases (eventually 2 GB) to support high transaction volumes and data-heavy applications, asserting it adhered more closely to Satoshi Nakamoto’s original vision.

-

Implications:

-

On-Chain Scalability:

-

BSV’s ability to handle large-scale transactions and applications demonstrated the potential of a high-capacity blockchain but raised concerns about network centralization, as fewer entities can afford to run nodes.

-

-

Fragmentation Risks:

-

Each fork diluted the community’s resources and focus, potentially slowing adoption and development compared to a unified approach.

-

The Evolution of Bitcoin’s Role

Original Vision vs. Reality:

Satoshi Nakamoto’s white paper described Bitcoin as a decentralized, peer-to-peer electronic cash system. However, BTC’s trajectory has focused on becoming digital gold—a store of value rather than a daily-use currency.

-

High fees and limited scalability on the base layer shifted BTC’s usability to long-term investment and large transactions, relying on Layer 2 solutions like the Lightning Network for smaller, faster payments.

Economic Implications of the Shift:

-

Inability to Replace Fiat Currencies:

-

With its current design, BTC cannot handle the transactional volume required to function as a global currency.

-

This leaves the fiat system intact, maintaining the monopoly of central banks and governments over monetary policy and capital controls.

-

-

Regulatory Leverage:

-

By not directly competing with fiat for everyday transactions, Bitcoin avoids triggering aggressive regulation aimed at preserving state control over money. This strategic positioning could be deliberate or a by-product of internal disagreements.

-

Centralisation Concerns:

While Bitcoin is decentralized in protocol, its ownership distribution and rising price challenge its founding ideals:

-

Ownership Concentration:

-

Studies reveal that 2% of wallets hold over 90% of Bitcoin’s supply. While some belong to exchanges holding BTC on behalf of users, the concentration among "whales" (large holders) raises concerns about market manipulation and influence.

-

-

Corporate and Government Accumulation:

-

Corporations like MicroStrategy and countries like El Salvador hold significant amounts of Bitcoin. If governments or other centralized entities acquire substantial holdings, they could:

-

Influence the market price by coordinating buying or selling strategies.

-

Use Bitcoin holdings as a tool to control or manipulate economies.

-

Undermine Bitcoin’s decentralization by concentrating ownership in fewer hands.

-

-

-

Impact on Retail Investors:

-

With BTC prices exceeding $90,000, owning a full Bitcoin is out of reach for most individuals, exacerbating economic inequalities and reinforcing its image as a "rich man’s asset."

-

Fractional ownership (satoshis) helps, but the psychological barrier of owning "just a fraction" may deter widespread adoption.

-

Long-Term Risks:

-

If a small number of entities control the majority of Bitcoin, they could limit its use as an alternative to fiat by:

-

Hoarding supply, reducing circulation.

-

Using their holdings to impose transaction restrictions or fees, undermining Bitcoin’s decentralized ethos.

-

A Hypothetical Alternative: Bitcoin as Scalable Electronic Cash

Had the community agreed to increase block sizes to enable on-chain scalability, Bitcoin could have developed as a global, decentralized payment system with implications such as:

-

Governments Losing Control Over Money:

-

Bitcoin could bypass traditional banking systems, enabling global transactions without government oversight.

-

This would challenge the ability of governments to:

-

Collect taxes on income or transactions.

-

Enforce capital controls, such as limiting money movement across borders.

-

Implement monetary policy, as citizens and businesses could opt out of fiat entirely.

-

-

-

Financial Inclusion:

-

With low transaction fees and high scalability, Bitcoin could serve as a practical payment method for the unbanked and underbanked, particularly in developing countries with unstable currencies.

-

This could reduce reliance on remittance services and create economic opportunities.

-

-

Marketplace Integration:

-

Scalable on-chain solutions could support decentralized marketplaces, where users buy and sell goods directly using Bitcoin without intermediaries like banks, credit cards, or centralized payment processors.

-

Challenges to Scalability:

-

Larger block sizes increase centralization risks by making node operation more resource-intensive.

-

Governments might aggressively regulate or ban Bitcoin if it competes directly with fiat.

Concluding Thoughts

The evolution of Bitcoin reflects the tension between decentralization, scalability, and adoption. While BTC’s shift toward digital gold ensures its survival as a store of value, it limits its potential as a peer-to-peer electronic cash system. Meanwhile, the rise of institutions and governments in Bitcoin ownership raises concerns about its decentralization and ability to challenge traditional financial systems.

A scalable Bitcoin could have profound implications, including reducing government control over money and enabling financial freedom. However, achieving this vision would require balancing technical feasibility, decentralization, and geopolitical realities—an ongoing challenge for the cryptocurrency community.

The Bitcoin Reformation

In The Bitcoin Reformation, the key idea is that Bitcoin is much more than a financial trend—it’s part of a broader revolution similar to the Protestant Reformation. Just like the Reformation shook up the old systems of power in 16th-century Europe, Bitcoin is challenging the modern financial system, particularly the control held by the International Monetary and Financial System (IMFS).

It starts with a historical parallel: during the Reformation, the Catholic Church held a monopoly on religious and spiritual services, which people began to rebel against. In a similar way, Bitcoin is offering a decentralized alternative to today’s centralized financial structures.

There are four main reasons why both movements took off:

-

Monopolistic Service Providers: The Catholic Church had control over spiritual matters just as the IMFS has control over global finance today. Bitcoin disrupts that, offering an alternative financial system.

-

Technological Revolution: The printing press was a game-changer in the 16th century, just like the internet, encryption, and Bitcoin are today. These new technologies make it easier for people to move away from centralized control.

-

A New Economic Class: Back then, it was the merchant class that pushed back against old power structures. Now, it’s millennials who are sceptical of traditional finance and embracing Bitcoin as an alternative.

-

Defence and Escape: Just as Dutch rebels used clever strategies to escape control (like flooding land to fight off invaders), today’s "rebels" are using cryptography and decentralized technologies to protect their privacy and financial assets.

Looking ahead, Bitcoin could transform the way we handle money. We might see the rise of full-reserve banking (similar to how banks operated in 17th-century Amsterdam), new forms of peer-to-peer insurance, and the widespread use of Bitcoin as collateral for loans. Derivatives markets around Bitcoin could also grow, just like they did in Amsterdam’s financial system during its Golden Age.

In conclusion, the idea here is that Bitcoin, much like the Reformation, represents a massive cultural shift. As more millennials gain economic power and continue to adopt Bitcoin, we could see a real challenge to the centralized financial systems that dominate today. Over time, Bitcoin has the potential to reshape the global economy just as the Reformation transformed Europe centuries ago.

This isn’t just about finance—it’s about a new way of thinking about money, privacy, and power in the digital age.

Bitcoin Knots

1. What is Bitcoin Knots?

- An alternative implementation of Bitcoin, derived from Bitcoin Core but with enhanced features.

- Provides more control over transaction policies, mempool management, and network filtering.

- Fully compatible with Bitcoin Core, allowing seamless switching between the two.

2. Key Features & Enhancements

- Advanced Transaction Filtering – Reject spam, dust, and inefficient transactions.

- Stricter Mempool Policies – Reduces blockchain bloat with settings like

Reject ParasitesandData Carrier Size. - Customizable Pruning – Handles blockchain storage dynamically based on available space.

- Faster Feature Adoption – Incorporates community-driven enhancements before they appear in Bitcoin Core.

3. Installation & Setup Notes (Start9 Box)

- Installed via Start9’s Marketplace (Bitcoin Knots 28.1.0).

- Initial install error: "Config Generation Error: No Match: blkconstr: Field Is Not Nullable".

- Resolution: A simple restart of the Start9 box allowed Knots to sync and run normally.

4. Post-Installation Verification

- Sparrow Wallet successfully connected to Bitcoin Knots.

- Last block synced correctly, mempool data displayed as expected.

- Lightning apps (LND, RTL) running without issues.

- Small test transaction sent successfully via Coldcard & Sparrow Wallet.

5. Key Takeaways

- Bitcoin Knots runs smoothly on Start9 after an initial restart.

- Advanced filtering features help keep the network efficient.

- Fully compatible with existing wallets & Lightning services.

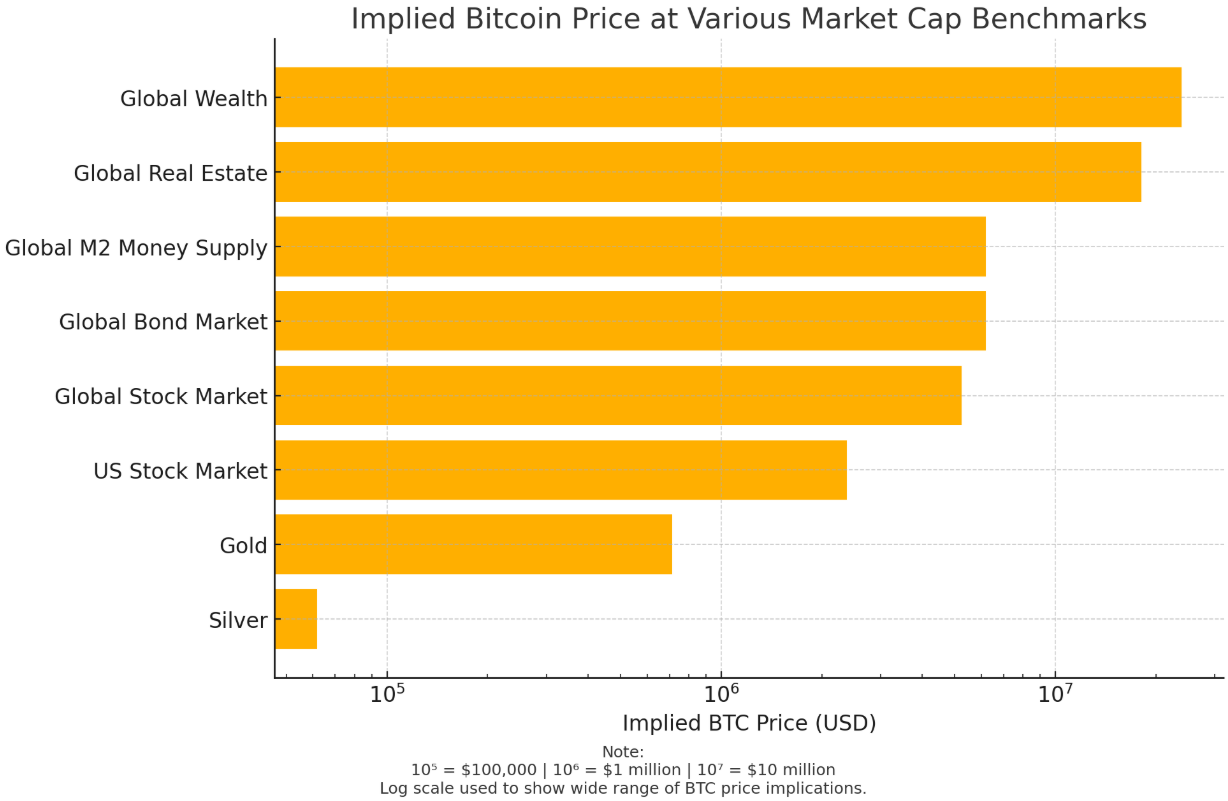

📊 Bitcoin Price Projections Based on Asset Class Market Caps

This chart visualises what the price of 1 Bitcoin (BTC) would be if Bitcoin’s total market cap grew to match various global asset classes.

Bitcoin’s supply is fixed at 21 million coins, making it inherently scarce. As demand grows and market adoption increases, Bitcoin’s market cap could—hypothetically—compete with other major stores of value.

💰 Asset Classes and Corresponding Implied BTC Prices

| Asset Class | Approx. Market Cap (USD) | Implied BTC Price |

|---|---|---|

| Silver | $1.3 trillion | ~$61,900 |

| Gold | $15 trillion | ~$714,000 |

| US Stock Market | $50 trillion | ~$2.38 million |

| Global Stock Market | $110 trillion | ~$5.23 million |

| Global Bond Market | $130 trillion | ~$6.19 million |

| Global M2 Money Supply | $130 trillion | ~$6.19 million |

| Global Real Estate | $380 trillion | ~$18.1 million |

| Total Global Wealth | $500 trillion | ~$23.8 million |

🧮 Calculation Method

Each BTC price is calculated by:

Implied BTC Price=Asset Class Market Cap21,000,000\text{Implied BTC Price} = \frac{\text{Asset Class Market Cap}}{21,000,000}Implied BTC Price=21,000,000Asset Class Market Cap

For example:

If Bitcoin reaches the size of gold’s market cap:

$15,000,000,000,000÷21,000,000≈$714,285\$15,000,000,000,000 ÷ 21,000,000 ≈ \$714,285$15,000,000,000,000÷21,000,000≈$714,285

🔢 Reading the Chart Scale

The X-axis uses a logarithmic scale to accommodate the wide price range:

-

10⁵ = $100,000

-

10⁶ = $1 million

-

10⁷ = $10 million

This helps show smaller values like silver without visually flattening the higher targets like real estate or global wealth.

🧠 Key Insight

Even reaching 10% of gold’s market cap would imply a BTC price over $70,000 — already within historical highs. The long-term upside remains significant due to Bitcoin’s absolute scarcity and growing global adoption.

📜 BIP-119 (CTV): A Potential Upgrade to Bitcoin

Status: Under discussion — could reach consensus by end of 2025

🔧 What is BIP-119 (OP_CHECKTEMPLATEVERIFY)?

-

Proposed in 2019 by developer Jeremy Rubin

-

Introduces a new opcode:

OP_CHECKTEMPLATEVERIFY(CTV) -

Enables covenants — restrictions on how and where Bitcoin can be spent

-

Unlocks vaults, congestion control, and more advanced smart contract-like behavior

🚀 Why It Matters

If adopted, BIP-119 could:

-

Improve self-custody: Vaults can limit withdrawals (e.g. max 0.1 BTC/week)

-

Strengthen Layer 2s: Helps support Eltoo-style channels in Lightning and Ark

-

Enhance scalability and security: Through congestion control and predefined transaction flows

-

Enable privacy tools: Such as discreet log contracts (DLCs) for conditional payments

🧠 Who Supports It?

A growing number of Bitcoin devs and orgs:

-

66 developers and firms signed an open letter (June 2025) urging adoption

-

Notable supporters:

-

Jameson Lopp

-

Andrew Poelstra

-

Engineers from Anchorage, Luxor Mining, Alpen Labs

-

-

Daniel Gray (Fidelity): “Covenants allow contracts too risky to do today”

-

Steven Roose (Second): Believes consensus could form by year-end

⏳ Upgrade Challenges

-

Bitcoin upgrades are slow by design

-

Changes must be backward-compatible (soft forks)

-

Taproot (2021) was the last upgrade — still controversial due to unforeseen uses (e.g. Ordinals)

-

Community seeks broad, cautious consensus before activation

🔐 What Are Covenants and Vaults?

Covenants: Limit how Bitcoin can be spent

-

Example: Prevent a vault from sending more than 0.1 BTC/week to a hot wallet

-

Can predefine:

-

Spending frequency

-

Destination addresses

-

Transaction structure

-

Vaults: Cold storage with enforced withdrawal logic

-

Adds an extra layer of protection

-

Useful for individuals and custodians alike

🔗 Broader Implications

-

Could help integrate Bitcoin with Ethereum-like smart contract systems

-

E.g., Avalanche, Arbitrum, Polygon

-

-

Supports Layer 2 bridges, better custody tools, and scaling solutions

📌 Conclusion

BIP-119 has the potential to:

-

Improve usability and security

-

Enable more sophisticated applications on Bitcoin

-

But requires broad consensus and thorough review

Activation possible by late 2025 — but not guaranteed.

Separation of Money and State

1. Central Banks Tighten Control

As citizens shift into parallel systems (Bitcoin, stablecoins, Web3 assets), central banks attempt to preserve fiat dominance:

-

Regulated on/off-ramps with strict KYC/AML.

-

Stablecoin licensing under central bank oversight.

-

Mandatory reporting of balances and transactions.

-

Crackdown on privacy tools and non-custodial wallets.

Goal: Close loopholes and keep citizens locked into fiat rails.

2. Adaptation as Trust in Fiat Erodes

Despite restrictions, adoption of non-state money continues. Governments adapt only to remain relevant:

-

CBDCs with programmable features and limited privacy tiers.

-

Tax gateways that accept BTC/stablecoins, converted instantly to fiat.

-

Treasury diversification in Bitcoin by corporates and some states.

-

Energy & trade settlements exploring Bitcoin as neutral collateral.

Effect: The state concedes parallel rails cannot be stopped, only delayed.

3. Gradual Separation of Money from the State

Citizens increasingly treat fiat as compliance money and Bitcoin as sovereignty money.

-

Fiat tolerated only for taxes and official obligations.

-

Parallel systems dominate savings, remittances, and peer-to-peer trade.

-

Exit pressure disciplines governments: abuse fiat, and citizens opt out.

4. The Endgame: Stateless Money, Protocol Governance

The gradual erosion of state control over money and governance itself:

-

Taxation power dissolves. Citizens allocate resources voluntarily; governments cannot finance wars or repression without consent.

-

Law decentralised. Property, contracts, and inheritance enforced on-chain by smart contracts and DAOs.

-

Military coercion fades. Collective security becomes DAO-driven; legitimacy flows from consensus, not force.

-

States reduced to services. Governments become optional providers competing with decentralised protocols.

5. Future Extension: Protocol-Run Society

Beyond the separation of money and state lies a deeper possibility:

-

Rules as Code: Governance routines embedded in smart contracts.

-

Consensus Enforcement: The blockchain itself enforces agreements, not courts or armies.

-

Voluntary Governance: Citizens choose which DAOs or protocols to align with, funding them transparently.

This vision transforms society itself into a protocol-run system, where rules are enforced by code and legitimacy is earned through voluntary participation.

The Weaker the Dollar, the Louder Bitcoin Roars

The Triffin Trap

The way the financial system used to work, and the dollar system was designed, is simple but devastating. When you are the world reserve currency, you operate inside what is called the Triffin dilemma. You can print the currency that everyone else must use to store value, settle trade, and price goods and services. But the price of that privilege is that you, the issuing state, must run deficits. And so the United States has run what is called the twin deficit—its greatest export is not technology or industry, but the currency itself. Year after year, dollars flow out, debt piles up, and the backbone of the economy—the middle class—shrinks. The wealth gap has never been larger.

Empire of Paper Promises

The solution is not to be the world’s reserve currency. That path has led to an empire of paper promises, bottomless debt, and weaponised inflation. The empire is now imploding under its own contradictions. What was once unthinkable is now admitted openly by those in power. The old playbook is dead. The world has entered a new battlefield.

Forced Tribute

In a shocking Fox News interview, Treasury Secretary Scott Bessent confessed that US allies like Japan, Korea, and Europe would be directed to recycle their trade surpluses back into America’s factories—to subsidise and finance America’s ability to produce. This is not cooperation; it is forced tribute. A 21st-century colonial plunder carried out in plain sight.

Strategic Suicide

And the admissions don’t stop there. The White House itself has begun saying what was once only whispered in think tanks: America can no longer afford to be dependent on the very rivals it claims to be preparing against. When Republicans and Democrats alike suddenly agree that the US must reshore production, rebuild factories, and stop outsourcing critical industries, it is not some rediscovered patriotism—it is because the benefits of the dollar system have run dry. What once sustained the empire has turned strategically suicidal. The United States cannot wage a prolonged conflict with a near-peer rival like China while still relying on Chinese rare earth minerals to build its missiles, tanks, and fighter jets. The contradiction is existential.

Hollowed Out

Other countries have an easier time because their labour is not priced in the world’s reserve currency—they can produce competitively without carrying the burden of being the issuer. America, by contrast, exported its industry in exchange for decades of cheap imports, but now finds itself hollowed out, with factories gone and a middle class that can no longer afford to buy what it once made.

The Intel Signal

That is why headlines about the White House allegedly considering taking a direct stake in Intel are not random market rumours but flashing red signals. The state is preparing to nationalise strategic industry through the back door. It is the clearest evidence yet that the old game of dollar hegemony is collapsing. The paper empire has reached the stage where it must cannibalise itself in order to survive.

The Case for Bitcoin

To reshore, America will print. Inflation at home and forced surplus recycling abroad are not separate policies — they are the same subsidy. The middle class pays with higher prices, and US allies in Europe and Asia pay with their savings. Together they bankroll an empire that can no longer fund itself honestly.

And so, the confessions pile up. What was long denied is now said openly: the system doesn’t work anymore. The Triffin dilemma is not an abstract textbook theory—it is a live detonation at the heart of the fiat order. Each step the US takes to “onshore” its economy only confirms the failure of the model. Every such admission makes the case for Bitcoin louder, sharper, more inevitable.

The End of the Fiat Empire

The scaffolding is coming down. The fiat empire is out of time. The post-1971 dollar is dead. The bull is awake.

🧭 The Full Bitcoin Club

Owning a Full Bitcoin in 2025 — What It Really Means

Owning one full Bitcoin has become something of a modern milestone — a symbolic threshold that represents both scarcity and conviction. According to a recent Cointelegraph analysis, fewer than a million blockchain addresses hold at least one Bitcoin. Once you account for exchanges, custodians, and individuals who spread their holdings across multiple wallets, the number of people who truly own a full Bitcoin is closer to 800,000–850,000.

In a world of roughly eight billion, that’s only about 0.01%–0.02% of the global population. Even among cryptocurrency holders, just 0.18% have one Bitcoin or more. The rest hold fractions. With more than 19.8 million BTC already mined and only 21 million ever to exist, scarcity is no longer an abstract concept — it’s measurable and undeniable.

The Evolution of Bitcoin’s Market Behaviour

What stands out in recent years is how Bitcoin’s volatility has diminished relative to its early cycles. The infamous “Bitcoin will go to zero” narrative has largely faded as the network and ecosystem have matured. Institutional participation — from corporations holding Bitcoin in reserves to the arrival of spot ETFs from BlackRock and Fidelity — has helped deepen liquidity and integrate Bitcoin into the broader financial system.

Volatility remains, but it is now contextualized. Even traditional markets have endured massive swings in recent years: the global pandemic, regional banking crises, and sovereign debt concerns have all shown that risk is not unique to crypto. The key difference is that Bitcoin’s supply can’t be inflated to address short-term economic or political pressure. That immutability is its defining strength.

Bitcoin vs. Gold: Sound Money for a Digital Age

Bitcoin is often compared to gold, and for good reason. Both are scarce, globally recognized, and free from direct government control. Yet I see Bitcoin as superior to gold on several fronts.

Gold is heavy, expensive to store, and difficult to transport or divide. Bitcoin, on the other hand, is infinitely divisible, instantly transferable, and self-custodiable. It removes the logistical and physical constraints that have limited gold’s monetary function in the digital era.

In many ways, gold was sound money for the physical age. Bitcoin is sound money for the digital one.

The Generational Shift

Younger generations — especially Gen Z — have grown up in a digital world where trust in traditional institutions has eroded. They’re comfortable with online platforms, cryptographic systems, and decentralized technology.

To them, Bitcoin is not “internet money”; it’s a transparent, verifiable system of value that doesn’t require permission to use. This mindset shift is profound. It suggests that the next generation may see Bitcoin less as an investment and more as the natural evolution of money itself.

The Inflation Illusion

We’re taught that inflation is a necessary part of a healthy economy. But is it? Inflation erodes the purchasing power of labour, silently taxing savers while rewarding debtors — especially governments that rely on debt issuance.

Bitcoin challenges that logic. Over time, its purchasing power has grown, while fiat’s has steadily declined. One Bitcoin today buys far more than it did five or ten years ago. The same cannot be said for any major fiat currency.

There’s a moral question here, too. Why should money — the product of human effort and energy — lose value by design? Inflation benefits those who create money, not those who earn it. It discourages saving and long-term thinking while rewarding leverage and speculation.

A monetary system where money retains its value — or even appreciates over time — encourages thrift, productivity, and sustainable growth. People would be happier, more secure, and more motivated to work, knowing their earnings are not being diluted by policy.

The Real Barrier: Misunderstanding Money

The biggest obstacle to Bitcoin adoption isn’t volatility — it’s a lack of understanding about what money truly is.

Most people focus on earning and spending but rarely question what gives money its value. We’ve been conditioned to believe that governments and central banks must manage money supply for the economy to function, even if that means devaluing currency over time.

Bitcoin flips that assumption. It proves that a monetary system can exist without intermediaries or central authorities — one where rules are transparent and immutable, not adjustable by decree. Value is preserved by mathematics, not by trust.

Systemic Resistance

Naturally, such a concept threatens the status quo. Governments and banks derive power from controlling the flow of money. That’s why we’re seeing more “protective” measures — transaction limits, delayed transfers, and tighter regulations around crypto purchases.

The stated goal is consumer safety, but the outcome is financial restriction. I’ve experienced it myself: sell Bitcoin, then try to buy back during a dip, and your bank may block the transaction. Whose money is it, really? (In such a scenario, these days you’d want to keep the funds in stablecoins, not fiat.)

These restrictions reveal something deeper — an unease with the idea of citizens having direct, permissionless access to a form of money outside institutional control.

A Quiet Monetary Revolution

Bitcoin is often described as an asset, but it’s more accurately a monetary revolution. It represents a shift from trust-based to truth-based systems — from centrally managed inflation to decentralized verification.

Owning one full Bitcoin isn’t about chasing wealth; it’s about aligning with a new standard of value — one that rewards time, effort, and prudence rather than debt and manipulation.